Blue carbon credits as a way to preserve the oceans

Today, it is no longer contested that human activities are causing global warming: the increased frequency of extreme weather events (heat waves, El Niño) or the Covid pandemic of the last two years are good examples. One of the mechanisms to mitigate global warming is carbon offsetting, through the purchase of carbon credits. It is commonly accepted that such credits can be acquired through the planting of trees. However, forests are not the source with the greatest potential for carbon sequestration: 55% of the CO2 captured by photosynthesis each year worldwide is captured by the oceans. The conservation and restoration of the oceans is therefore essential to maintain acceptable living conditions on our planet.

By Pierre-Emmanuel GUILHEMSANS-VENDÉ, R&D Consultant at TNP Consultants. With the contribution of Lionel POURCHIER and Frédéric FAVRE, Founders of Blue Leaf Conservation

A very slow increase in awareness

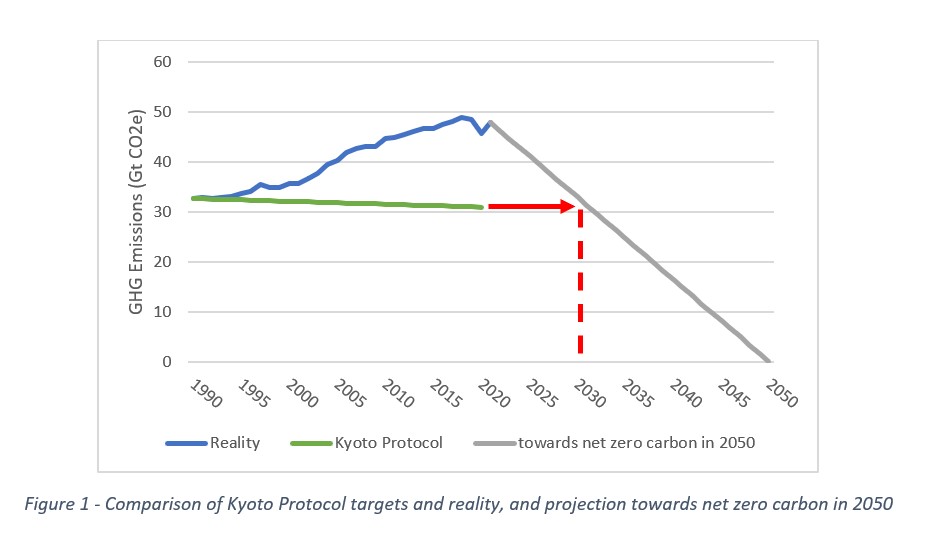

Since March 21, 1994, the United Nations Framework Convention on Climate Change (UNFCCC) has officially recognized the existence of climate change and the responsability of humans for it. This convention has since been ratified by 195 countries, called “Parties”. In 1995, an annual meeting of the UNFCCC signatory states was established: the Conference of the Parties (COP). In 1997, the Kyoto Protocol, aimed at reducing greenhouse gas (GHG) emissions, was signed at COP 3. GHG emissions had to be reduced by 5.2% by 2020 with 1990 as the base year (for the EU, 8 %). The EU did reduce its greenhouse gas (GHG) emissions by 23% between 1990 and 2018 and thus exceeded its target… but at the global level, emissions increased by 67% [1]. Thus, although the phenomenon is theoretically recognized, in reality awareness is slow and, despite all the mechanisms put in place to mitigate global warming, emissions have never stopped increasing (see Figure 1).

In 2015, at COP 21, the Paris Agreement was signed. The aim is to limit global warming to below 2°C, preferably 1.5°C. The objective of a net zero level by 2050 is stated, i.e. a net zero emissions balance. Why limit the increase to 2°C or even 1.5°C? There are many reasons for this, such as limiting rising sea levels, biodiversity loss, extreme weather events… and more pragmatically, +2°C is equivalent to a 0.2 to 2% drop in global income each year according to the 2014 IPCC report [2]. In 2006, Nicholas Stern had already warned that the cost of inaction against global warming would be a 5 to 20% drop in global GDP compared to only 1% for action! [3]

We must therefore drastically reduce our emissions and even aim to be at net zero by 2050 to limit global warming to below 2°C. It should also be noted that the emissions reduction target by 2030 corresponds to the global objective of the Kyoto Protocol: we must achieve in 10 years what could not be done in 30 years (with an annual reduction corresponding to the total reduction over 30 years)! This is a very ambitious goal!

What are the mechanisms to mitigate global warming?

But what are the existing solutions that would allow us to reach this objective?

To answer this question, there are currently three global mechanisms to reduce CO2 emissions:

- Carbon markets

There are two types of carbon markets: compliance markets (in the EU, the Emission Trading System or ETS) and voluntary markets. Fit for 55 plans to include shipping (3.3%), road transport (17%) and buildings (14%) in the EU ETS from 2025 onwards, which would increase the percentage of EU emissions covered by the EU ETS from 45% to around 75%. [4]

- National or multinational regulations/initiatives outside the EU ETS

For example, within the EU, GHG reduction targets are effectively set for sectors covered by the EU ETS but also for non-EU ETS sectors.

| Climate & Energy package 2021-2030 (2014) | Fit for 55 package (2021) | |

| GHG emissions from 1990 to 2030 | – 40 % | – 55 % |

| Renewable energies share in 2030 | 27 % | 40 % |

| Primary energy consumption | – 27 % | – 40 % |

| GHG emissions in EU ETS sectors: 2005-2030 | – 43 % | – 61 % |

| GHG emissions in non-EU ETS sectors : 2005-2030 | – 30 % | – 40 % |

- Green bonds

Green bonds are a kind of bond issued on the financial markets by a company or a public entity in order to finance sustainable development projects. For example, the French national railway SNCF issues green bonds to finance the purchase of new trains or the maintenance of existing trains, as trains are 30 times less polluting than cars (60 times less than air travel).

Of these three mechanisms, we will focus on carbon markets, and more specifically on voluntary markets. Compliance markets will be discussed in another article.

Voluntary markets: anyone can contribute

The first voluntary markets were created in 1996, following the second IPCC report, but they only really took off in 2006, with the creation of voluntary standards[5]. The voluntary standards were inspired by the requirements of Kyoto certification (JI/CDM), adapting them to reduce the time and cost of certification. They were created to provide assurance, transparency, and credibility to voluntary market credits. There are 14 main voluntary standards identified by Ecosystem MarketPlace: Verra, GS, ACR, CAR, CARB, Plan Vivo, ProClima, Climate Forward, ART TREES, CDM, City Forest Credits, Coalition for Rainforest Nations, EcoRegistry, Global Carbon Council. But in reality, two of these standards accounted for the majority of sales in 2021: Verra and GS.

. The objective of voluntary markets is to reduce GHG emissions by offering an alternative to compliance markets, which are accessible to a limited number of actors. Theyr are based on a voluntary approach: there is no obligation, and anyone can contribute. Only one mechanism is used: the financing of offset projects.

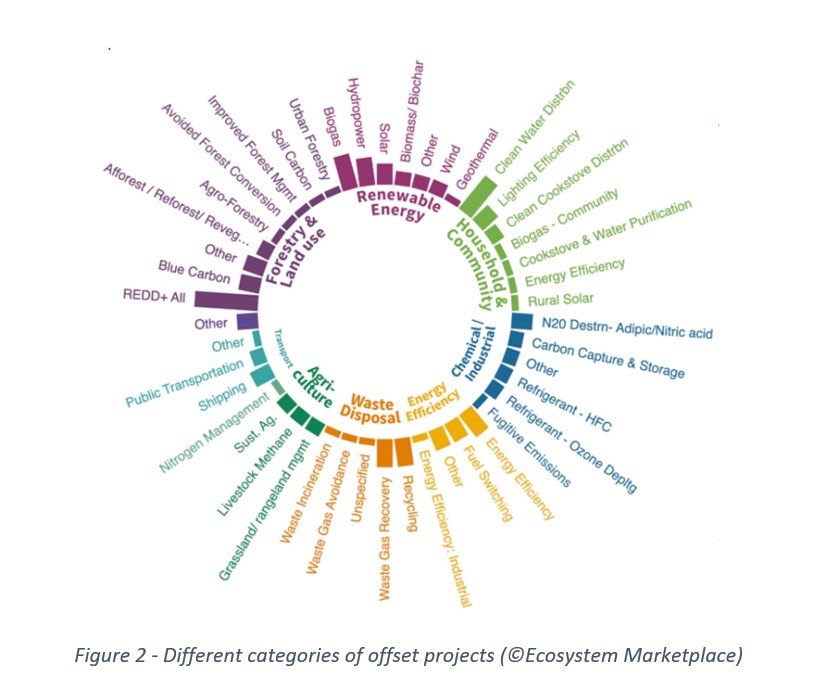

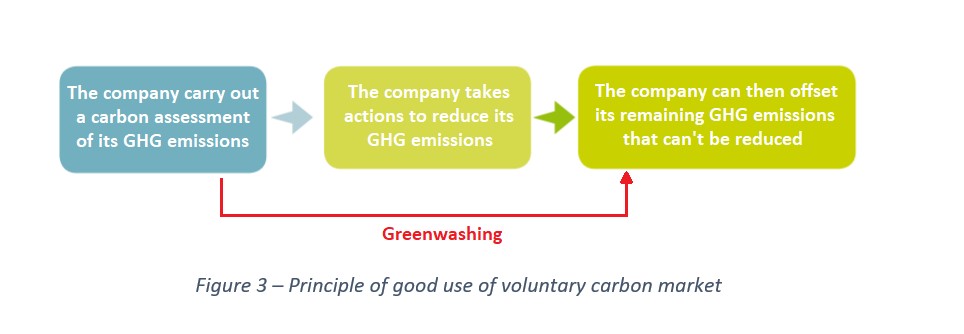

These projects can reduce GHG emissions (more efficient and/or low-carbon technology, such as hydrogen buses) or involve sequestration: for example, planting trees, using CO2 as a refrigerant, or burying it in the ground. All the categories of offset projects can be found in Figure 2. However, before being able to offset (or contribute, a term that has become very fashionable lately) and to respect the ARC principle (Avoid, Reduce, Compensate) as much as possible, the purchaser must first carry out a carbon assessment of its GHG emissions and take actions to reduce its GHG emissions. Only then will it be legitimate in his offsetting approach: otherwise, this is called greenwashing (see Figure 3).

The voluntary market, with more than 3,600 projects since its inception [6], has been growing steadily, particularly over the last three years. In 2021, the annual value of the market exceeded one billion euros for the first time in its history and even peaked at 1.985 billion euros

The original currency here is the dollar, but as the parity between euro and dollar is currently around one, due to the conflict between Russia and Ukraine and the recent complete shutdown of the Nord Stream 1 pipeline by Russia’s Gazprom, the choice has been made here to put everything in euros.

The original currency here is the dollar, but as the parity between euro and dollar is currently around one, due to the conflict between Russia and Ukraine and the recent complete shutdown of the Nord Stream 1 pipeline by Russia’s Gazprom, the choice has been made here to put everything in euros.

. This is a great evolution of the market, as the second largest capitalization occurred in 2008 (2020 being only third). The cumulative size and value of the market from its inception to the end of 2021 is 1.982 Gt of avoided GHG emissions and eight billion euros, according to Ecosystem Marketplace, with a quarter of that achieved in 2021 alone [7].

In these carbon offset projects, the unit used is the carbon credit: one credit corresponds to tone metric ton of CO2 equivalent. The average price of a carbon credit was €4 in 2021, 60 % more than in 2020. This inflationary trend in the voluntary market will most likely continue and even increase as demand is expected to exceed supply by 2025. The most popular projects are related to forestry and land use (see Figure 2), accounting for more than 46 % of traded volumes and 67 % of market value in 2021. However, renewable energy projects have been gaining momentum since 2019, with equivalent or even higher volumes and sharply rising prices – +109% from 2020 to 2021 – whereas forestry projects are showing little change: +7% from 2020 to 2021. The majority of projects (65% in 2021) involve the reforestation, restoration or safeguarding of forests: these can be called green carbon credits. According to Ecosystem Marketplace, these carbon credits sell for around €5.80 each. As an individual, this type of carbon credit is easily accessible via several online platforms such as EcoTree, Olive Gaea, Coforest, MyTree or 8 Billion Trees, at prices that are nonetheless much higher and variable (€1.67 to €36 per tree and €11 to €36 per credit, depending on the type of tree, its geolocation and whether it lives 20 years or a century and beyond).

Blue carbon credits: a very promising market

Green carbon credits are thus the most developed form of carbon offset and the best known by the general public, and often synonymous with greenwashing. However, they are not the source with the greatest potential for carbon sequestration: 55% of the CO2 captured by photosynthesis each year in the world is captured by the oceans, hence the name blue carbon. Moreover, coastal ecosystems (mangroves, seagrass beds and tidal marshes), while covering only 0.2% of the world’s ocean surface, alone store 46.9% of this blue carbon in ocean sediments. These ecosystems have a carbon sequestration rate 30 to 50 times higher than that of forests [8]. Nevertheless, until now, blue carbon has been under-exploited, with only a few projects resulting from the protection of mangroves.

It is in this context that the start-up BlueLeaf Conservation (BLC) [9], founded by Lionel POURCHER and Frédéric FAVRE, and partner of TNP since April 2022, is playing a role. BLC is currently developing a pilot project to monitor Posidonia meadows in the Bay of Cannes in collaboration with the NGO Nature Dive – which plants Posidonia meadows and participates in awareness-raising and education on the subject –,along with the city, urban area and trust of Cannes. The idea is to be able to determine a model linking hectares of Posidonia with tons of CO2 and then certify this methodology via the French low carbon standard. Between 0 and 15 m, the monitoring of seagrass beds could be done via satellite (beyond that, between 15 and 40 m, there are problems of luminosity). In addition, there is a scientific obstacle to the development of a generalizable satellite recognition tool (depending on the coastline studied, there will be a multifactorial variation in the image to be analyzed).

The methodology approved via the French low carbon standard could lead to the delivery of carbon credits, made up of 80% for the protection of the existing meadows and 20% for restoration.

It is necessary to mobilize and federate stakeholders to ensure the financing of conservation and restoration projects for marine ecosystems. These potential stakeholders include private companies, but also Green Climate Funds, international donors, states, and local authorities. For the moment, organizations and governments are reluctant to invest in marine conservation projects in the absence of a clear and proven carbon footprint methodology. Moreover, there is no consensus on a single voluntary standard that would allow certification costs to be lowered by volume effect, and thus lower the cost of blue carbon credits and make them more attractive. Lionel proposes the creation of an online platform, linked to a new entity named EverSea, to connect the various stakeholders, encourage project financing, facilitate the process of carbon credit certification, and provide access to tools and methods for monitoring marine ecosystems. On the one hand, NGOs and marine area managers will be able to find marine ecosystem monitoring services (combination of different techniques) and carbon credit certification services. On the other hand, companies wishing to mitigate their CO2 emissions as part of their CSR policy will be able to offset their emissions by purchasing blue carbon credits directly on the platform and transparently monitor the results of the projects they finance through this mechanism. This transparent monitoring will be guaranteed thanks to blockchain technology.

Theoretically, the offset mechanism proposed by EverSea is virtuous and goes in the right direction, by proposing to monetize ecosystems that have been highly damaged until now because they were wrongly considered renewable, infinite and without interest. In practice, EverSea will have to deal with many climat hazards: ocean acidification, rising sea levels, increased land-based flooding and hurricanes that can damage mangroves and salt marshes… All these phenomena will jeopardize the survival of these ocean assets. However, we must encourage the proliferation of companies involved in the conservation and restoration of terrestrial and marine biodiversity, by promoting the sustainability of their business models. This will require banks to take global warming into account in their financing and insurance risk management. At the same time, companies will have to reduce their carbon footprints, by steering their ESG policies through an internal carbon price or by making green investments, for example through Time for the Planet with its climate dividends. These notions of climate dividends and internal carbon price will be the subject of a future article.

Sources

[1] “’Fit for 55’: un nouveau cycle de politiques européennes pour le climat”, RPUE – Représentation Permanente de la France auprès de l’Union européenne, July 15, 2021.

[2] GIEC, “Changements climatiques : rapport de synthèse”, 2014.

[3] N. Stern, “The Economics of Climate Change: The Stern Review”, Oct. 2006.

[4] “Fit for 55 : la Commission européenne revoit l’ensemble de sa politique climat à l’aune de sa nouvelle ambition pour 2030”, Citepa, July 15, 2021.

[5] ADEME, “La compensation volontaire : démarches et limites”, June 2012.

[6] “Carbon Credit Projects & Transactions”, Trove Intelligence. https://trove-intelligence.com

[7] Ecosystem MarketPlace Insights Brief, “The Art of Integrity: State of the Voluntary Carbon Markets 2022 Q3”, August 2022.

[8] C. M. Duarte, I. J. Losada, I. Hendriks, I. Mazarrasa, and N. Marba, “The role of coastal plant communities for climate change mitigation and adaptation”, Nature Climate Change, October 29, 2013.

[9] L. Pourchier and F. Favre, “Blue Leaf Conservation website”. https://blueleafconservation.com/